All Categories

Featured

Table of Contents

Fixed-rate options are also readily available, with their own maximum spreads. The government-backed warranty is what makes these rates competitive relative to most alternative or online loaning items. The SBA does not provide straight. Owners apply through an SBA-approved lending institution, who finances the loan based upon its requirements and SBA standards.

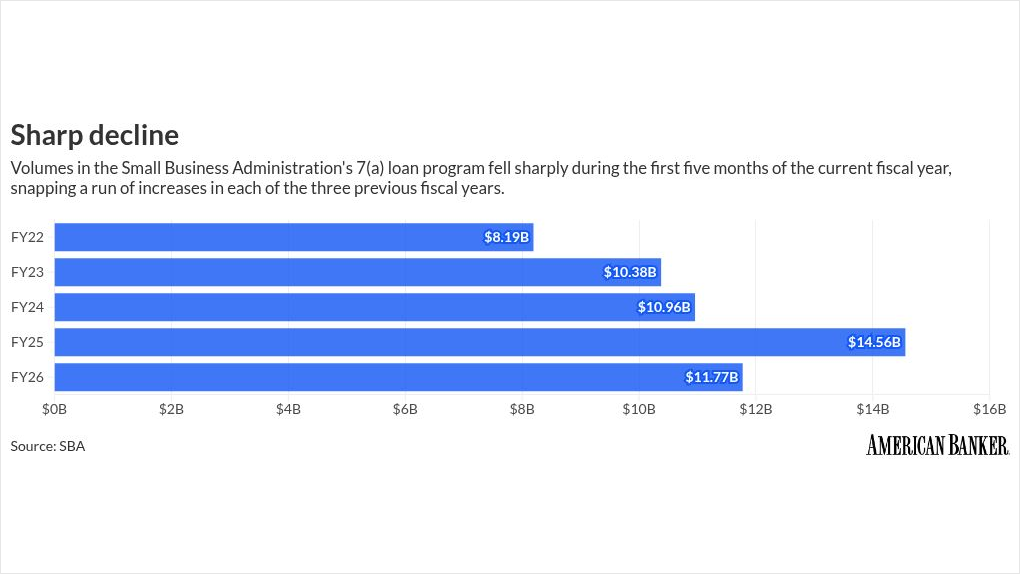

Using a lender with an established SBA department, like a credit union with industrial lending sta, can signicantly enhance the process The scale of SBA financing reects how commonly services throughout the country rely on the program. That volume was driven in part by strong growth in the 7(a) program's smallest loan tier, those under $150,000, reecting demand from early-stage and smaller businesses that may otherwise struggle to access standard nancing.

Little service owners often rst think about big nationwide banks for loans due to their name acknowledgment and branch existence. Owners often nd bigger institutions have more stringent approval standards, less exible underwriting, and an impersonal experience. Credit unions, in contrast, run dierently, as information programs. The Federal Reserve's 2026 Report on Employer Firms, based upon the 2025 Small Business Credit Survey, discovered that candidates who sought nancing at little banks were more most likely to be totally authorized at 57% than those who looked for nancing from any other kind of lender.

By contrast, 60% of borrowers who acquired nancing through online lenders reported that real loaning expenses were greater than anticipated, while only 32% of large bank debtors and 37% of little bank customers said the very same. Smaller, relationship-based organizations regularly deliver better results and less unwelcome surprises on cost. As not-for-prot, member-owned organizations, cooperative credit union oer organization customers more competitive loan prices, exible underwriting, and a much deeper understanding of the member's company.

How to Manage Small Business AccountingPost-closing, the relationship component continues, resulting in greater debtor satisfaction than with online or large lending institutions, according to a Federal Reserve study. Access to a dedicated industrial financing expert who examines the application and preserves continuity adds worth not totally caught by aggregate information. For customers, this worth extends even more, as cooperative credit union loans are generally exempt from intangible tax, offering a meaningful reduction in closing costs compared to other lending institutions.

How to Manage Small Business AccountingUsing Automation to Boost Store Financial Planning

According to the Federal Reserve's 2026 Small company Credit Study, applicants at little banks were fully authorized at a rate of57%, outperforming large banks and online loan providers. Credit union candidates reported comparable approval results with greater fulfillment. Debtors at little institutions were far less likely to encounter higher-than-expected loaning expenses compared to online ntech lenders, where 60% reported costs above anticipation.

Credit rating is one of the rst things a lender evaluates when reviewing a business loan application, and one of the most common reasons applications get rejected. For SBA loans specically, personal credit scores usually need to be 650 or above for basic qualication, with more powerful applications showing 680 or greater, per Rating's assistance on personal credit and company loan approval.

Navigating Key Business Funding Requirements in 2026

A denial from one loan provider does not imply nancing is impossible. Dealing with a lender that utilizes a relationship-based underwriting technique, rather than rigorous automated rating thresholds, allows a company owner's complete nancial photo to be assessed. Service credit report, kept by bureaus like Dun & Bradstreet, Experian Company, and Equifax Company, are separate from individual scores.

Developing a business credit prole early, even with small supplier accounts or a service credit card, signicantly strengthens future loan applications. Till recently, loan providers were required to prescreen smaller SBA loan applications utilizing the FICO Small Service Scoring Service rating, known as the SBSS.

Company owners pursuing SBA nancing must ask their lending institution directly which scoring models they use and what thresholds they use internally. According to a LendingTree analysis of Federal Reserve lending information, debtor nancials were the main factor pointed out for company loan denials in Q1 2025, with 68.4% of companies noting this as the cause, followed by credit report at 21.5% and absence of collateral at 5.7%.

{kind=link}

Latest Posts

Is Operational Automation the Key to Reduce Costs?

Smart Staff Scheduling Strategies for Peak Productivity

Improving Store Operations for Financial Success